Income tax Form 26AS “A Tax credit Statement”

1. Introduction:

Form 26AS or Tax credit statement is one of the basic documents, required to file an Income tax return of the person. It gives a consolidated record of each tax-related transaction and information associated with the PAN (Permanent Account Number) of the assessee. The income information available in form 26AS should be reconciled with the income tax return of the taxpayer.

2. What is Form 26AS:

From 26AS is a consolidated statement of tax deducted at the source and tax collected at the source of a person which is deposited with the government. Other than details of TDS and TCS it also provides some other information of transactions done by the taxpayer in the particular financial year. The transaction comprises Advance tax/self-assessment tax/ Regular Assessment Tax deposited, Refund, specified financial transactions, etc.

3. Details and Information available in Form 26AS:

It is a consolidated Information Statement which contains the details of transactions for a particular Financial Year (FY). It contains the following details in its different parts:

Part I:

It contains the details regarding Tax Deducted at the source which includes the Name and TAN of the Deductor, Total Amount Paid/credited, Tax Deducted, and Total TDS Deposited.

Tax deducted on income from salary, contract, Interest income, etc. are displayed in this part of the Form.

Part II:

It contains the details regarding Tax Deducted at Source in cases where Form 15G / 15H has been submitted by the deductee.

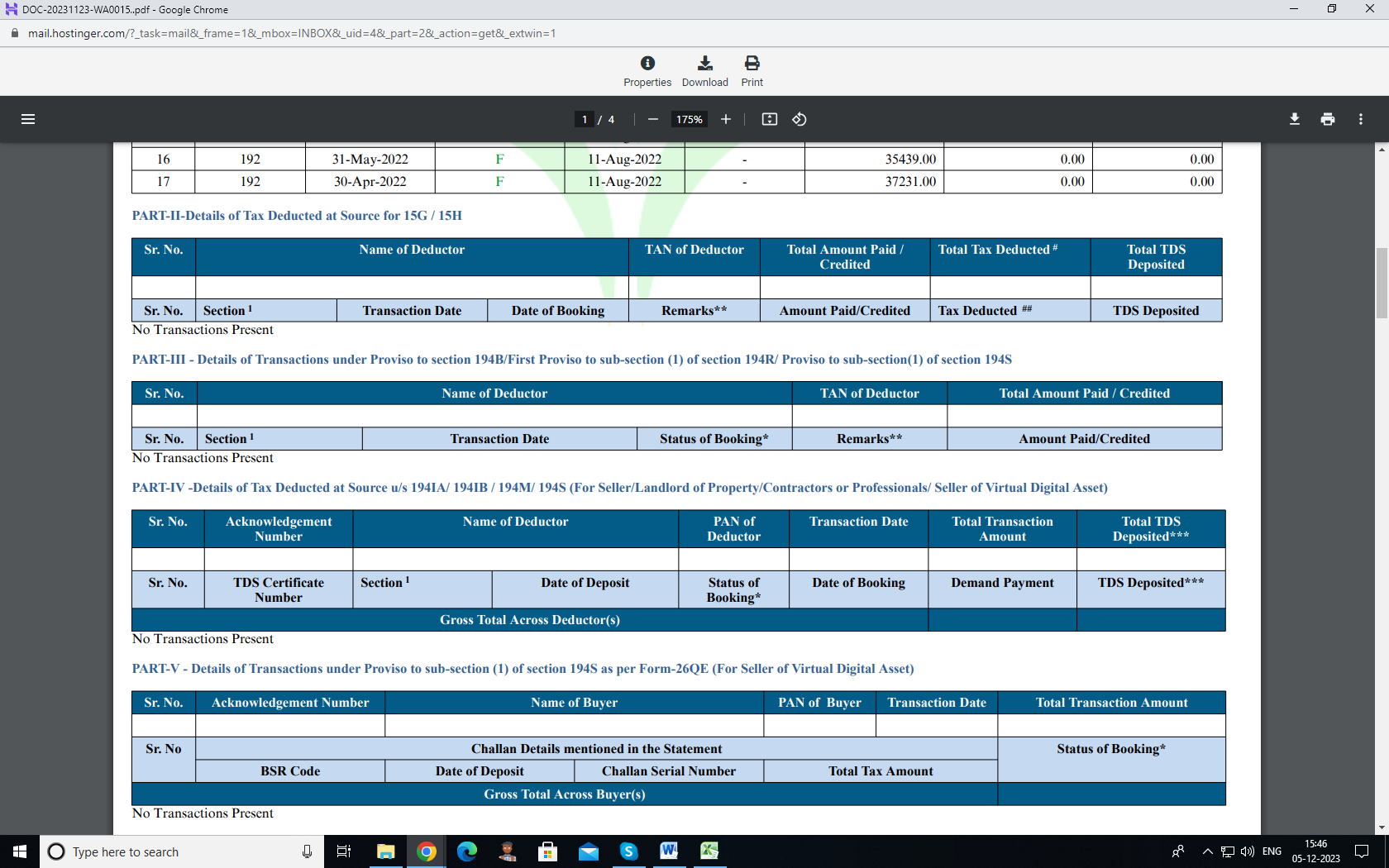

PART-III –

It provides the details of Transactions under Proviso to section 194B/First Proviso to sub-section (1) of section 194R/ Proviso to sub-section(1) of section 194S. i.e winnings from lotteries, game shows, card games, online games, crossword puzzles, quiz shows, benefit or perquisite in respect of business or profession partly in cash partly in kind, transaction regarding virtual digital assets

PART-IV

It contains details regarding Tax Deducted at Source u/s 194IA/ 194IB / 194M/ 194S (For Seller/Landlord of Property/Contractors or Professionals/ Seller of Virtual Digital Asset)

These details are provided in Form 26AS of a taxpayer who is the seller of the immovable property, landlord of the property, or contractors or seller of the VDA.

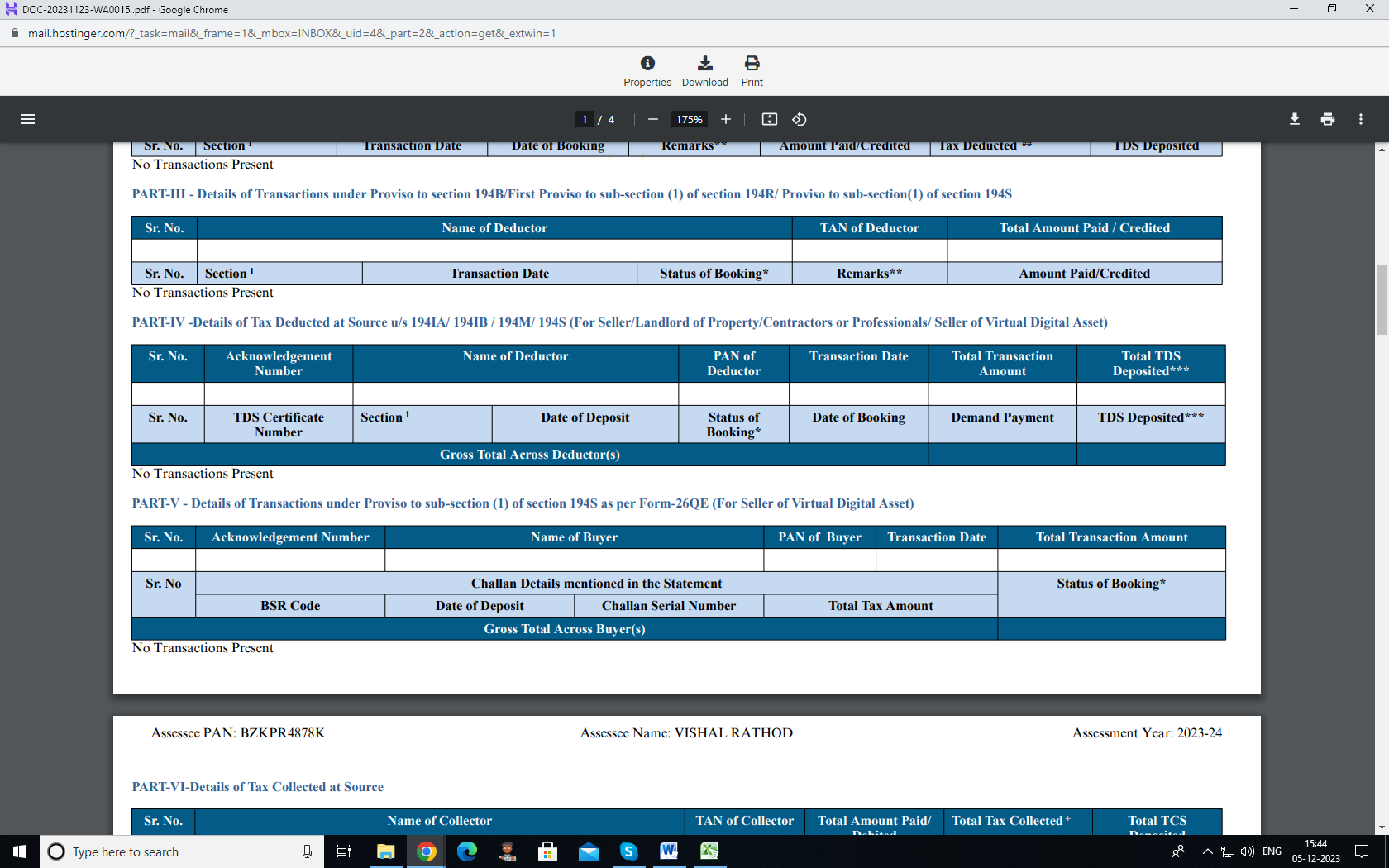

PART-V

It provides the details of Transactions under Proviso to sub-section (1) of section 194S as per Form-26QE (For Seller of Virtual Digital Asset) i.e. transactions regarding virtual digital assets

PART-VI

It gives details of Tax Collected at Source.

PART-VII

It provides details of Refund Paid (For which source is CPC TDS. For other details refer to AIS at the E-filing portal). Refund paid to assesse during the financial year reflects in this part of Form 26AS

PART-VIII

It contains details of Tax Deducted at Source u/s 194IA/ 194IB /194M/194S (For Buyer/Tenant of Property /Person making payment to contractors or Professionals / Buyer of Virtual Digital Asset)

Transactions related to Immovable property, like purchase, TDS on rent paid to landlord, payment to contractor u/s 194 or payment for VDA u/s 194S beyond the specified limit.

These details are provided in Form 26AS of a taxpayer who is the buyer of the immovable property, tenant of the property, or payer to contractors or buyer of the VDA.

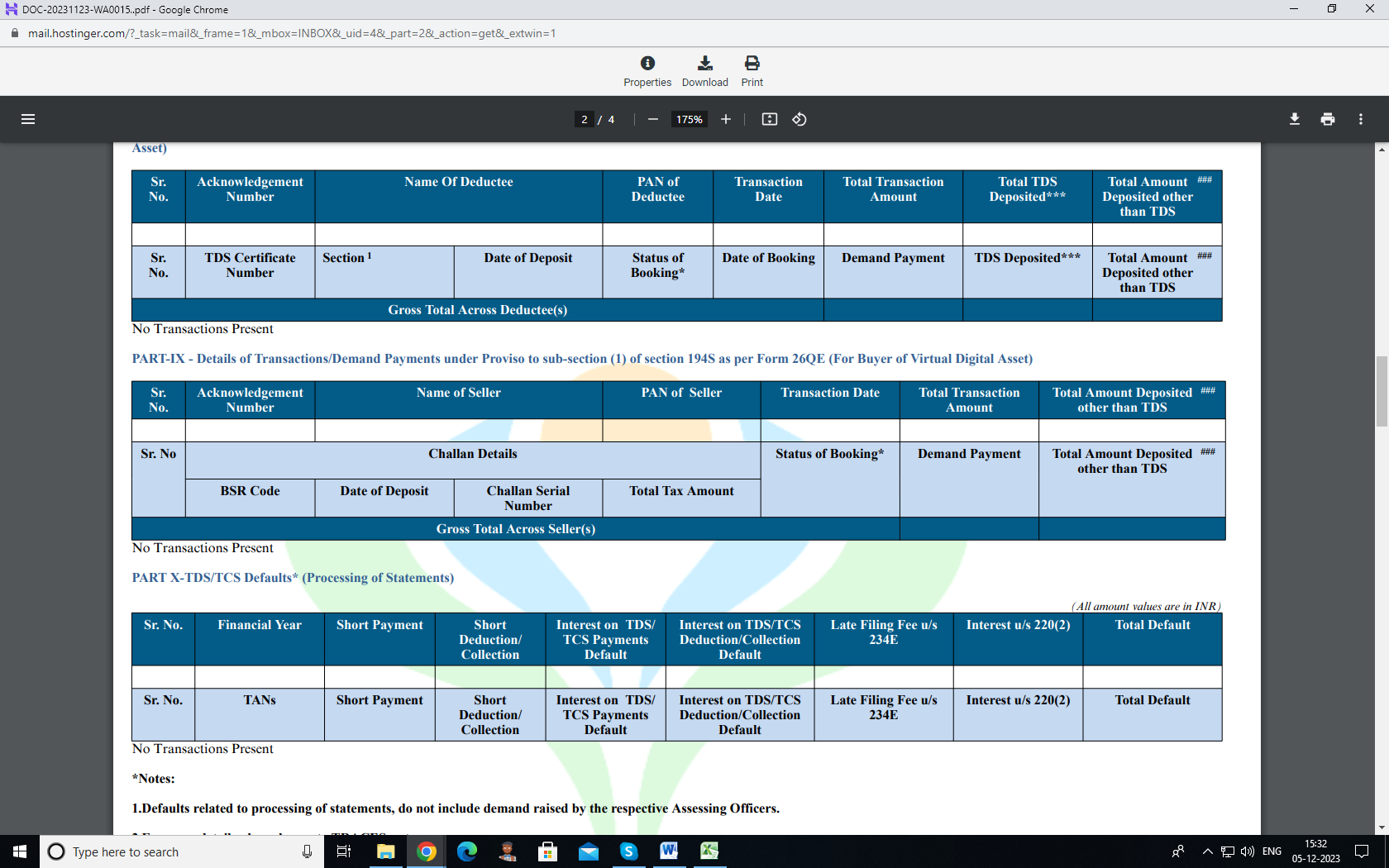

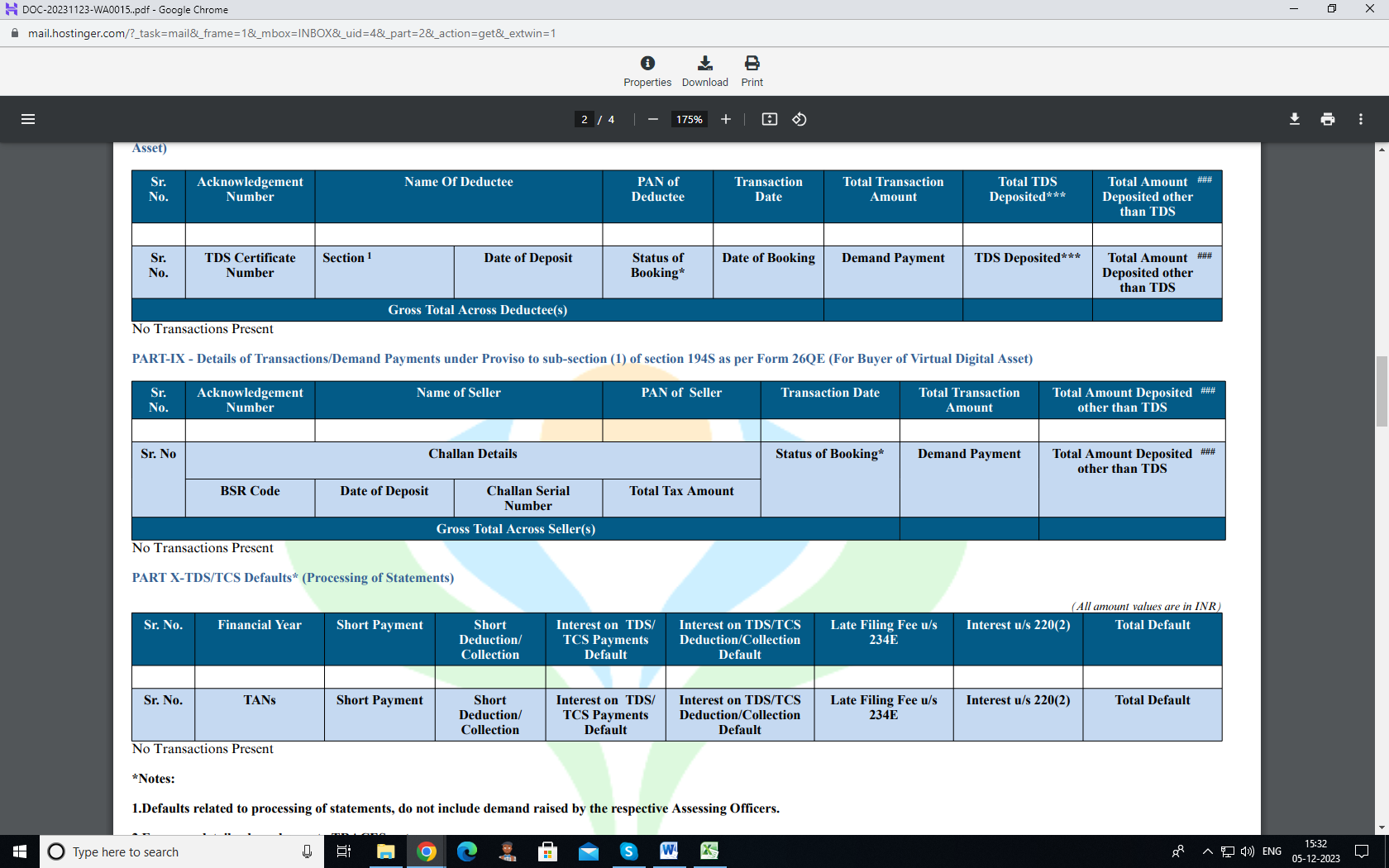

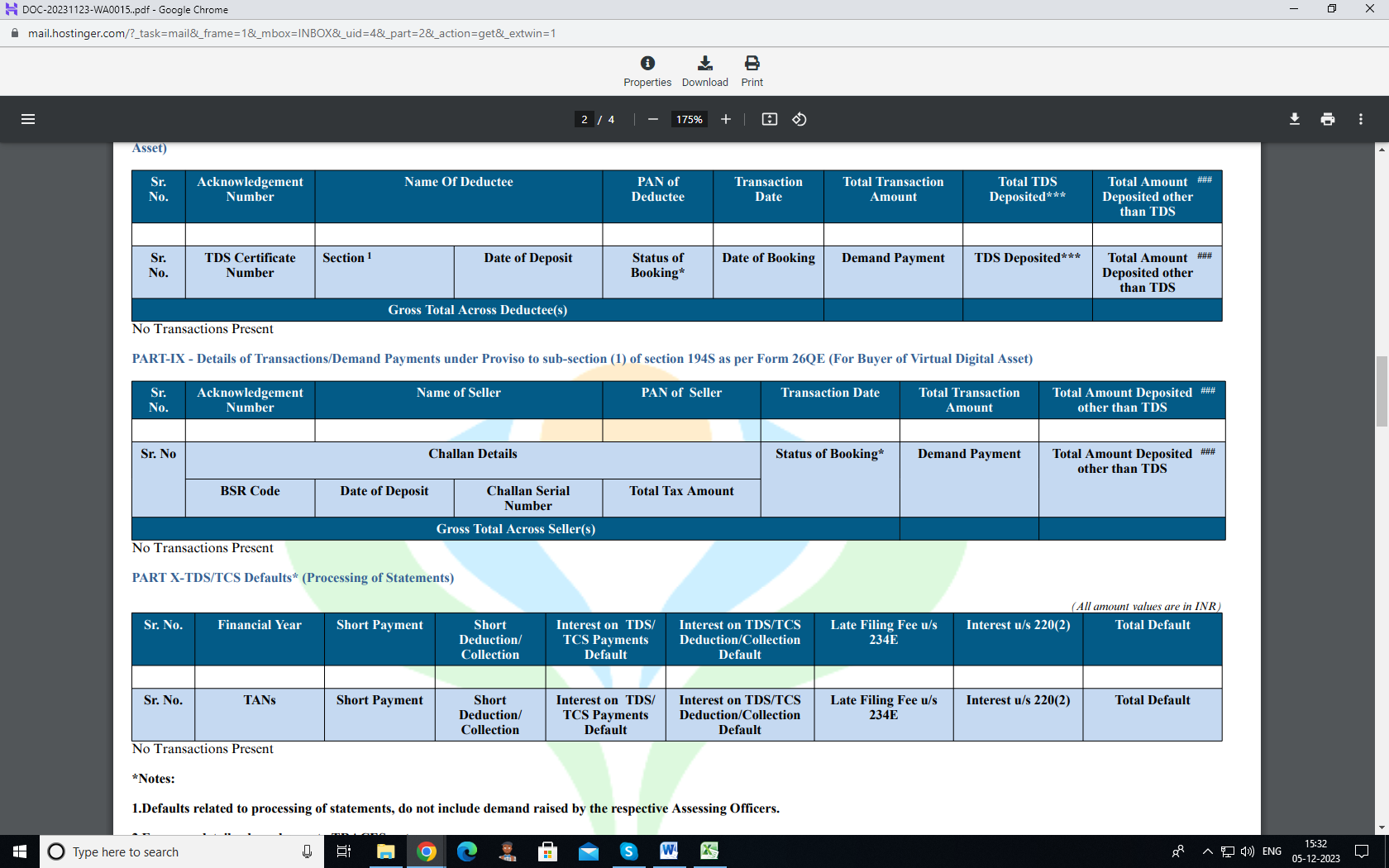

PART-IX

It gives details of Transactions/Demand Payments under Proviso to sub-section (1) of section 194S as per Form 26QE (For Buyer of Virtual Digital Asset)

PART X

TDS/TCS Defaults (Processing of Statements):

4. How to View or Download Tax Credit Statement (Form 26AS)

Taxpayers can view or download Form 26AS from the e-filing portal by following the steps given below:

- Step1: Log in to ‘e-Filing’ Portal https://www.incometax.gov.in/iec/foportal/

- Step2: Go to the 'e-file'> Income Tax Returns and click on 'View Form 26AS”.

- Step3: Read the disclaimer, click 'Confirm' and the user will be redirected to TDS-CPC Portal.

- Step4: In the TDS-CPC Portal, Agree the acceptance of usage. Click 'Proceed'.

- Step5: Click ‘View Tax Credit (Form 26AS)’ and Select the ‘Assessment Year’

- Step6: Select the ‘View type’ (HTML, Text or PDF)

- Step7: Click ‘View / Download’ (To export the Tax Credit Statement as PDF, view it as HTML > click on 'Export as PDF'.)

5. TDS Deducted and TDS Credited to Form 26AS

The taxpayer should reconcile the TDS deducted with the TDS credited to Form 26AS. If it does not match or the TDS credited in Form 26AS is less than the actual TDS deducted. Then in this case the occurrence of discrepancy may be due to reasons like non-furnishing of TDS details to the IT Department by the deductor, deducting the tax in incorrect PAN, etc. If a discrepancy is due to the deductor, then the taxpayer should ask the deductor to correct the same.

6. Conclusion:

All taxpayers should reconcile the income and Tax information declared in the ITR with Form 26AS before filing the Income tax return for the relevant year. The discrepancy may lead to litigation or other repercussions. Form 26AS is a statement of information which is in possession of the department. The compliance with law can prevent from the penalties and other litigations.

Disclaimer:-The information available on this website/Application is solely for informational purposes. We make no representation or warranties of any kind, express or implied about the accuracy, reliability, with respect to information and material or video available on website/Application, any reliance you place on such information is therefore strictly at your own risk. We are not liable for any consequence of any action taken by you relying on the material/information provided on this website/Application

GST Revenue collection for November 2023 is ₹1,67,929 lakh crore. This marks the record highest growth rate of 15% Y-o-Y The gross GST revenue collection for the month of November, 2023 is ₹1,67,929 crore.

The gross GST revenue collection for the month of November, 2023 is ₹1,67,929 crore.

The bifurcation of GST Revenue collection is as below :-

| Particulars | Amount |

| CGST | ₹30,420 crore |

| SGST | ₹38,226 crore |

| IGST | ₹87,009 crore (including ₹39,198 crore collected on import of goods) |

| CESS | ₹12,274 crore (including ₹ 1,036 crore collected on import of goods) |

| Total | ₹1,67,929 crore |

The GST revenue collection for November 2023 is 15% higher than the GST revenue collection in the same month last year and the highest for any month year-on-year during 2023-24, up to November 2023.

This is the Sixth time in FY 2023-24, where Gross GST collection crosses ₹1.60 lakh crore. This signals a sign of a robust economy and proves that India is doing well economically.

There is impressive growth in GST collection, it is higher by 11.9% Year on year for FY2023-24 upto November, 2023

During the month, the revenues from domestic transactions (including import of services) are 20% higher than the revenues from these sources during the same month last year.

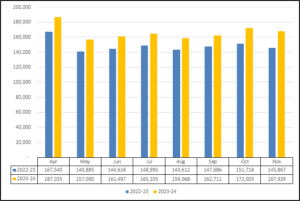

The gross GST collection for the FY 2023-24 upto November, 2023 is ₹13,32,440 crore, (Average ₹1.66 lakh per month. If we compare with the last year's same period, Gross GST collection for the FY 2022-23 up to November, 2022 was ₹11,90,920 crore (Average ₹1.49 lakh crore per month).

Comparison chart of GST collection for the FY 2023-24 upto November 2023 & FY 2022-23 upto November 2022

State-wise growth of GST Revenues during November, 2023[1]

| State/UT | Nov-22 | Nov-23 | Growth (%) |

| Jammu and Kashmir | 430 | 469 | 9% |

| Himachal Pradesh | 672 | 802 | 19% |

| Punjab | 1,669 | 2,265 | 36% |

| Chandigarh | 175 | 210 | 20% |

| Uttarakhand | 1,280 | 1,601 | 25% |

| Haryana | 6,769 | 9,732 | 44% |

| Delhi | 4,566 | 5,347 | 17% |

| Rajasthan | 3,618 | 4,682 | 29% |

| Uttar Pradesh | 7,254 | 8,973 | 24% |

| Bihar | 1,317 | 1,388 | 5% |

| Sikkim | 209 | 234 | 12% |

| Arunachal Pradesh | 62 | 92 | 48% |

| Nagaland | 34 | 67 | 99% |

| Manipur | 50 | 40 | -21% |

| Mizoram | 24 | 33 | 37% |

| Tripura | 60 | 83 | 39% |

| Meghalaya | 162 | 163 | 1% |

| Assam | 1,080 | 1,232 | 14% |

| West Bengal | 4,371 | 4,915 | 12% |

| Jharkhand | 2,551 | 2,633 | 3% |

| Odisha | 4,162 | 4,295 | 3% |

| Chhattisgarh | 2,448 | 2,936 | 20% |

| Madhya Pradesh | 2,890 | 3,646 | 26% |

| Gujarat | 9,333 | 10,853 | 16% |

| Dadra and Nagar Haveli and Daman & Diu | 305 | 333 | 9% |

| Maharashtra | 21,611 | 25,585 | 18% |

| Karnataka | 10,238 | 11,970 | 17% |

| Goa | 447 | 503 | 12% |

| Lakshadweep | 0 | 0 | -15% |

| Kerala | 2,094 | 2,515 | 20% |

| Tamil Nadu | 8,551 | 10,255 | 20% |

| Puducherry | 209 | 228 | 9% |

| Andaman and Nicobar Islands | 23 | 31 | 37% |

| Telangana | 4,228 | 4,986 | 18% |

| Andhra Pradesh | 3,134 | 4,093 | 31% |

| Ladakh | 50 | 62 | 25% |

| Other Territory | 184 | 222 | 21% |

| Center Jurisdiction | 154 | 223 | 45% |

| Grand Total | 1,06,416 | 1,27,695 | 20% |

SGST & SGST portion of IGST settled to States/UTs

April-November (Rs. crore)

| Pre-Settlement SGST | Post-Settlement SGST[2] | |||||

| State/UT | 2022-23 | 2023-24 | Growth | 2022-23 | 2023-24 | Growth |

| Jammu and Kashmir | 1,513 | 1,960 | 30% | 4,892 | 5,367 | 10% |

| Himachal Pradesh | 1,547 | 1,731 | 12% | 3,838 | 3,701 | -4% |

| Punjab | 5,102 | 5,612 | 10% | 12,906 | 14,734 | 14% |

| Chandigarh | 401 | 439 | 9% | 1,414 | 1,505 | 6% |

| Uttarakhand | 3,193 | 3,625 | 14% | 5,157 | 5,586 | 8% |

| Haryana | 12,052 | 13,415 | 11% | 20,761 | 23,134 | 11% |

| Delhi | 9,127 | 10,340 | 13% | 19,202 | 21,037 | 10% |

| Rajasthan | 10,146 | 11,348 | 12% | 22,853 | 25,699 | 12% |

| Uttar Pradesh | 17,924 | 21,624 | 21% | 43,951 | 49,282 | 12% |

| Bihar | 4,715 | 5,377 | 14% | 15,672 | 16,991 | 8% |

| Sikkim | 202 | 321 | 59% | 558 | 677 | 21% |

| Arunachal Pradesh | 311 | 418 | 34% | 1,059 | 1,276 | 21% |

| Nagaland | 138 | 206 | 49% | 635 | 701 | 10% |

| Manipur | 190 | 229 | 20% | 924 | 730 | -21% |

| Mizoram | 117 | 182 | 56% | 557 | 634 | 14% |

| Tripura | 272 | 335 | 23% | 955 | 1,037 | 9% |

| Meghalaya | 298 | 394 | 32% | 961 | 1,103 | 15% |

| Assam | 3,379 | 3,885 | 15% | 8,236 | 9,553 | 16% |

| West Bengal | 14,298 | 15,600 | 9% | 25,878 | 28,042 | 8% |

| Jharkhand | 4,947 | 5,866 | 19% | 7,374 | 8,116 | 10% |

| Odisha | 9,279 | 10,626 | 15% | 12,486 | 15,515 | 24% |

| Chhattisgarh | 4,838 | 5,398 | 12% | 7,366 | 8,831 | 20% |

| Madhya Pradesh | 6,979 | 8,496 | 22% | 17,772 | 20,673 | 16% |

| Gujarat | 24,753 | 27,671 | 12% | 37,497 | 41,545 | 11% |

| Dadra and Nagar Haveli and Daman and Diu | 427 | 426 | 0% | 792 | 699 | -12% |

| Maharashtra | 55,650 | 65,983 | 19% | 84,633 | 96,551 | 14% |

| Karnataka | 23,026 | 26,713 | 16% | 43,152 | 48,766 | 13% |

| Goa | 1,272 | 1,487 | 17% | 2,325 | 2,616 | 13% |

| Lakshadweep | 6 | 16 | 157% | 20 | 69 | 239% |

| Kerala | 8,005 | 9,171 | 15% | 19,657 | 20,623 | 5% |

| Tamil Nadu | 23,802 | 27,046 | 14% | 38,849 | 42,472 | 9% |

| Puducherry | 308 | 330 | 7% | 793 | 933 | 18% |

| Andaman and Nicobar Islands | 123 | 140 | 14% | 322 | 347 | 8% |

| Telangana | 10,926 | 12,994 | 19% | 24,460 | 26,691 | 9% |

| Andhra Pradesh | 8,325 | 9,291 | 12% | 18,742 | 20,952 | 12% |

| Ladakh | 111 | 155 | 40% | 378 | 457 | 21% |

| Other Territory | 114 | 156 | 37% | 329 | 702 | 113% |

| Grand Total | 2,67,818 | 3,09,003 | 15% | 5,07,355 | 5,67,464 | 12% |

Disclaimer:-The information available on this website/ App is solely for informational purposes. We make no representation or warranties of any kind, express or implied about the accuracy, reliability, with respect to information and material or video available on website/APP, any reliance you place on such information is therefore strictly at your own risk. We are not liable for any consequence of any action taken by you relying on the material/information provided on this website.

What is Section 143(1)

Section 143(1) of the Income Tax Act outlines the processing procedure for returns filed under Section 139 or in response to a notice issued under Section 142(1). This assessment is complete without calling the assessee. This is also known as Summary-assessment, Preliminary Assessment. This may also called as a system-generated assessment based on various information collected by the income tax department form AIS / TIS / 26AS / SFT etc. This notice is typically generated by the mainframe system to highlight visible mistakes in the submitted return. It specifically focuses on errors that are readily identified through the automated processing system.

Procedure of assessment under section 143(1)

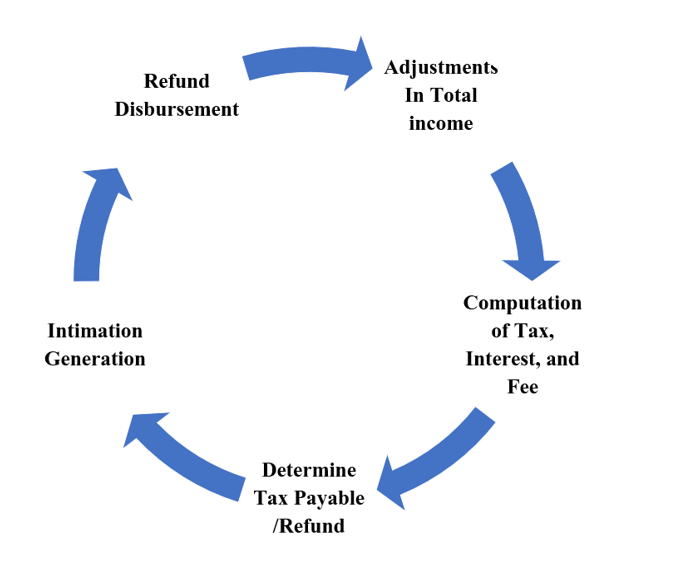

The processing involves a series of adjustments to compute the total income or loss as shown in the diagram.

What are Adjustments made In Total income?

- Rectify the arithmetical errors in the return.

- Correcting any apparent incorrect claims identified from the information in the return.

- Disallowing the claimed loss if the return for the relevant previous year, for which the loss set off is sought, was filed beyond the due date specified in Section 139(1).

- Disallowing any expenditure or additional income indicated in the audit report but not reported in the total income computation in your return.

- Disallowing deductions claimed u/s 10AA or provisions of Chapter VI-A related to deductions for certain incomes if the return is filed after the due date specified in Section 139(1).

- Adding income reported in Form 26AS, Form 16A, or Form 16, STF etc. which has not been incorporated in the total income computation in the return.

Section 143(1) ensures that returns undergo thorough processing, addressing errors, correcting claims, and making necessary adjustments to arrive at the accurate total income or loss.

Time-limit

Assessment under section 143(1) can be made within a period of 9 months from the end of the financial year in which the return of income is filed.

Question : Whether any action to be taken by the assesssee if no intimation is received till the expiry of one year?

Reply : No, in Such Case Your ITR–V acknowledgment will be deemed your intimation.

Types of intimation

- Intimation with No Demand or No Refund

- Intimation with Demand

- Intimation with Refund

How to deal with Intimation under Section 143(1)

Receiving an Intimation under Section 143(1) can be a routine part of the assessment process. Here's a step-by-step process for dealing with Intimation received

- Review the Intimation

- Understand Adjustments

- Verify Information: Cross-Check with Form 26AS/TIS/AIS

- Examine & Compare Deductions and Exemptions

- Reconcile Payments of Tax in Income tax Return & Under Intimation

- Professional Advice if Needed

- Respond within Timelines if discrepancies with income tax return

- Rectify Errors

- Keep Records of response

Password to open intimation u/s 143(1)?

To open the intimation under Section 143(1), it is essential to input the correct password. This security measure ensures secure access to the file, safeguarding the confidentiality of the information contained within. The password for these files is your PAN number in lowercase and your date of birth or date of incorporation in DDMMYYYY format. For example, if your PAN number is AARIK7108R and your date of birth is 10 October 1983, then the password will be ‘aarik7108r10101983’.

Can to get the Intimation u/s 143(1) again?

Steps to Download Intimation Order After Income Tax Return Processing:

Visit the official e-Filing Portal of Income Tax

Redirect to 'Income Tax Returns':

- Go to the 'e-file' section

- Select 'Income Tax Returns.'

- Click on 'View Filed Returns' to proceed

- Download Intimation Order

By following these steps, you can easily download the Intimation Order after the processing of your Income Tax Return by the Centralized Processing Centre (CPC).

Centralized Processing Centre [CPC] & It’s Role

The Government of India (GOI) on the recommendations of the Business Process Re-engineering Committee (BPR Committee) approved (February 2009) the establishment of a Centralised Processing Centre.

The Income Tax Department has been granted the authority to establish a Centralized Processing Center (CPC) dedicated to handling tax returns. The primary goal of this center, is to determine the tax liability and process refunds for taxpayers.

Notably, the CPC autonomously processes returns submitted by assesses without any involvement from the taxpayer or jurisdictional officers. This streamlined approach aims to ensure swift and accurate processing of returns while providing timely information to taxpayers.

Upon the completion of the processing phase, the department issues an intimation to the taxpayer. This intimation serves as a communication channel, allowing the taxpayer an opportunity to respond to any adjustments made by the CPC. It is crucial for the taxpayer to address these adjustments within 30 days of receiving the intimation.

Disclaimer:-The information available on this website/ App is solely for informational purposes. We make no representation or warranties of any kind, express or implied about the accuracy, reliability, with respect to information and material or video available on website/APP, any reliance you place on such information is therefore strictly at your own risk. We are not liable for any consequence of any action taken by you relying on the material/information provided on this website.

GSTR-9 is an Annual return to be filed by every registered person whose aggregate turnover is more than Rs. 2 crore.GSTR 9 is a compilation of GSTR 1, GSTR 3B, GSTR 2A, and inward & outward supply for the respective financial year.

GSTR-9 is required to be filed by every registered person having an aggregate turnover of more than Rs. 2 crore. However, the following persons are not required to file GSTR-9.

- Input service distributor.

- Casual taxable person.

- Non-resident taxable person.

- Tax deductor.

- Tax collector.

- OIDAR service provider who is located in a non-taxable territory.

Provided that the Commissioner may, on the recommendations of the Council, by notification, exempt any class of registered persons from filing annual returns under this section.

Due Date of Filing of Annual Return.

The due date to file GSTR-9 for a financial year is 31st of December of the following year.

For Example – The due date for filing of annual return for F.Y. 2022-23 is 31st December 2023.

Some other Important Points Before the Filing of Annual Return.

Before filing the annual return, ensure that all applicable returns such as GSTR -1 and GSTR- 3 have been filed.

Once the annual return is filed, no changes can be made. Also, you have to keep in mind that in a financial year, if you were registered in the composition scheme for some months and in the remaining months you are registered in the normal scheme, then you will have to file an annual return for the composition scheme also. It means, in this case, it is necessary to file both returns. i.e. GSTR -4 and GSTR-9.

GSTR-9 is divided into six parts :-

- Basic Detail.

- Details of Outward and inward supplies made during the financial year.

- Details of ITC for the financial year.

- Details of tax paid as declared in returns filed during the financial year.

- Particulars of the transactions for the financial year are declared in returns of the next financial year till the specified period.

- Other Information.

Now, we shall understand in depth, how to file GSTR-9

Table Number 4 – Details of advances, inward and outward supplies made during the financial year on which tax is payable.

Point- 4 (A) - Supplies made to un-registered persons (B2C) – In this table, during the financial year, any supply made to unregistered persons are submitted. These figures are auto-populated from GSTR-1. Auto-populated data can be cross-checked through filed GSTR -1 or IFF.

Point - 4(B) Supplies made to registered persons- During the financial year, any supply made to registered persons. Such details are submitted here. These figures are auto-populated from GSTR-1. Auto-populated data can be cross-checked through filed GSTR-1 and IFF.

Point - 4(C) - Zero rated supply (Export) on payment of tax (except supplies to SEZs)- Aggregate value of exports (except supplies to SEZs) on which tax has been paid shall be declared here. Table 6A of FORM GSTR-1 may be used for filling up these details.

Point - 4(D) - Supply to SEZs on payment of tax – During the financial year, any supply made to SEZ unit, such details are furnished in point D. Table 6B of GSTR-1 may be used for filling up these details.

Point 4 (E) - Deemed Exports - Details of Deemed Exports made during the financial year submitted in point E. Table 6C of FORM GSTR-1 may be used for filling up these details.

Point - 4(F) - Advances on which tax has been paid but the invoice has not been issued (not covered under (A) to (E) above)- During the financial year, supplies on which tax has been paid but invoices have not been issued and such advances are not covered from point A to point E are to be reported here. Table 11A of FORM GSTR-1 may be used for filling up these details.

Point – 4(G) - Inward supplies on which tax is to be paid on a reverse charge basis- Details of such inward supplies have to be submitted where tax has been paid in the Reverse Charge Mechanism.

Point - 4(H) - Sub-total (A to G above)- In Point H, the sub-total from Point A to Point G will auto-populate.

Point – 4(I) - Credit Notes issued in respect of transactions specified in (B) to (E) above – In Point I, details related to credit note has been issued in respect of transactions specified from Point B to Point E are required to be submitted.

Point – 4( J) - Debit Notes issued in respect of transactions specified in (B) to (E) above - In Point J, details related to debit note issued in respect of transactions specified from point B to point E are required to be submitted.

Point- 4 (K) - Supplies/tax declared through Amendments- In Point K, details of supply declared through amendment are required to be submitted.

Point- 4 (L) - Supplies/tax reduced through Amendments – In point L, details of supply reduced through amendment required to be submitted.

Point- 4 (M) - Sub-total (I to L above) – In Point M, the Subtotal from Point I to Point L will auto-populate.

Point- 4 (N) - Supplies and advances on which tax is to be paid (H + M) above – Point N is a sub-total of Point H and Point M. In this point details are auto-populated.

Table No. 5 - Details of Outward supplies made during the financial year on which tax is not payable –

Outward supplies made during the financial year on which tax is not payable, details of such supplies are to be submitted in this table. In this table, data will be auto-populated based on the return filed. You can check the auto-populated data from your books of accounts. If the data does not match, then you can change it.

Point 5 -(A) - Zero-rated supply (Export) without payment of tax- In Point A, details of supply made through LUT (Zero-rated supply) are to be submitted here. FORM GSTR-1, Table six A can be used to fill details in Point-A.

Point 5(B)- Supply to SEZs without payment of tax- Details of Supply made to special economic zone unit without payment of tax are to be submitted here. FORM GSTR-1, Table six B can be used to fill details in Point-B.

Point 5(C) - Supplies on which tax is to be paid by the recipient on a reverse charge basis- Where the buyer (recipient) is liable to pay tax under RCM, such details are required to be submitted here. FORM GSTR-1, Table four B can be used to fill details in Point C.

Point 5(D) - Exempted- In point D, Details of exempted supply have to be submitted. FORM GSTR-1, Table eight can be used to fill details in Point D.

Point 5(E) - Nil-Rated- In Point E, details of the Nil-rated supply are required to be submitted.

Point 5(F) - Non-GST supply (includes ‘no supply’) – Details of Supplies that are outside the scope of GST are to be submitted here. FORM GSTR-1, Table eight can be used to fill details in Point F.

Point 5(G) - Sub-total (A to F above) - In point G, the sub-total amount from Point A to Point F is auto-populated.

Point 5(H) - Credit Notes issued in respect of transactions specified in A to F above - Any credit note issued In respect of the Transaction specified from point A to F, such details have to be submitted here.

Point 5(I) - Debit Notes issued in respect of transactions specified in A to F above – Any debit note issued in respect of the Transaction specified from point A to F, such details have to be submitted here.

Point 5(J) - Supplies declared through Amendments - Supply declared through amendment have to be submitted in Point J.

Point 5(K) - Supplies reduced through Amendments - In Point K, supply reduced through amendment such details have to be furnished here.

Point 5(L) - Sub-Total (H to K above) - In point L, Point H to K sub-total amount is auto-populated.

Point 5(M) - Turnover on which tax is not to be paid (G + L above) - In Point M, Point G and L sub-total amount is auto-populated.

Point 5(N)- Total Turnover (including advances) (4N + 5M - 4G above): In Point N, Total Turnover including advances is auto-populated from point N of table number four and point M of table number five. But, subtract inward supplies on which tax is to be paid on a reverse charge basis.

Part – III Details of ITC availed during the financial year- During the financial year, details of ITC and the Breakdown of such ITC have to be shown here.

Point 6(A) - Total amount of input tax credit availed through FORM GSTR-3B (sum total of Table 4A of FORM GSTR-3B) - In Point A, the Total input tax credit availed in Table 4A of FORM GSTR-3B for the taxpayer is auto-populated.

Point 6(B) - Inward supplies (other than imports and inward supplies liable to reverse charge but includes services received from SEZs) - Aggregate value of input tax credit availed on all inward supplies except those on which tax is payable on reverse charge basis but includes supply of services received from SEZs shall be declared here.

Point 6(C)- Inward supplies received from unregistered persons liable to reverse charge (other than B above) on which tax is paid & ITC availed- Aggregate value of input tax credit availed on all inward supplies received from unregistered persons (other than import of services) on which tax is payable on reverse charge basis shall be declared here. Table 4(A) (3) of FORM GSTR-3B may be used for filling up these details.

Point 6(D)- Inward supplies received from Inputs registered persons liable to reverse charge (other than B above) on which tax is paid and ITC availed- Aggregate value of input tax credit availed on all inward supplies received from registered persons on which tax is payable on reverse charge basis shall be declared here. Table 4(A) (3) of FORM GSTR-3B may be used for filling up these details.

Point 6(E) - Import of goods (including supplies from SEZs) - Details of input tax credit availed on import of goods including supply of goods received from SEZs shall be declared here. Table 4(A) (1) of FORM GSTR-3B may be used for filling up these details.

Point 6(F) - Import of services (excluding inward supplies from SEZs): Details of input tax credit availed on import of services (excluding inward supplies from SEZs) shall be declared here. Table 4(A) (2) of FORM GSTR3B may be used for filling up these details.

Point 6(G) - Input Tax credit received from ISD- Aggregate value of ITC received from input service distributor shall be declared here. Table 4(A) (4) of FORM GSTR-3B may be used for filling up these details.

Point 6(H) - Amount of ITC reclaimed (other than B above) under the provisions of the Act- Aggregate value of ITC, reversed and reclaimed under the provisions of the Act shall be declared here.

Point 6(I) - Sub-total (B to H above) - In Point I, sub- total amount is auto-populated from Point B to H.

Point 6(J)- Difference (I - A above)- By subtracting Point A from Point I, the difference will be auto-populated here.

Point 6(K) - Transition Credit through TRAN-I (including revisions if any) - ITC is available through Tran–I. Its details are to be shown here. Also, if any revision has been done then it will also be included.

Point 6(L) - Transition Credit through TRAN-II - ITC availed through Tran -II. Its details are to be shown here.

Point 6(M) - Any other ITC availed but not specified above- ITC availed but not covered in any of the heads specified under 6B to 6L above shall be declared here.

Point 6(N) - Sub-total (K to M above) – In Point N, the sub-total amount is auto-populated from Point K to M.

Point 6(O) - Total ITC availed (I + N above) - During the year, whatever ITC we have availed will be auto-populated here.

Table No. 7 - Details of ITC Reversed and Ineligible ITC for the financial year-

Point 7(A) As per Rule 37- If the consideration is not paid, within the prescribed time. Due to this ITC has been reversed, then its details have to be submitted here.

Point 7(B) - As per Rule 39- Rule 39 determines the procedures for distributing ITC to input service distributors. If ITC is reversed as per rule 39, then its details have to be entered here.

Point 7(C) - As per Rule 42- During the financial year, if taxable supply, non-taxable supply, and exempt supply are made and ITC is used for non-business and personal purposes. Then the ITC used for non-business and personal purposes will have to be reversed. As per Rule 42, the details of the reversed ITC have to be entered here.

Point 7(D) -As per Rule 43- Rule 43 talks about determining ITC on capital goods or ITC reversal. If you have reversed ITC as per Rule 43 then its details have to be entered here.

Point 7(E) As per section 17(5) - If ITC is reversed as per section 17(5). Then its details have to be entered here.

Point 7(F) Reversal of TRAN-I credit - ITC is reversed due to TRAN -I. Its details have to be entered here.

Point 7(G) Reversal of TRAN-II credit- ITC is reversed due to TRAN -II. Its details have to be entered here.

Point 7(H) Other reversals (pl. specify) - ITC which has been reversed during the year. And such ITC is not covered anywhere. Its details have to be entered here.

Point 7(I) Total ITC Reversed (Sum of A to H above) - ITC reversed from point A to point H will be auto-populated here.

Point 7(J) Net ITC Available for Utilization (6O - 7I) - ITC which is available for Utilization. Its total will auto-populate here.

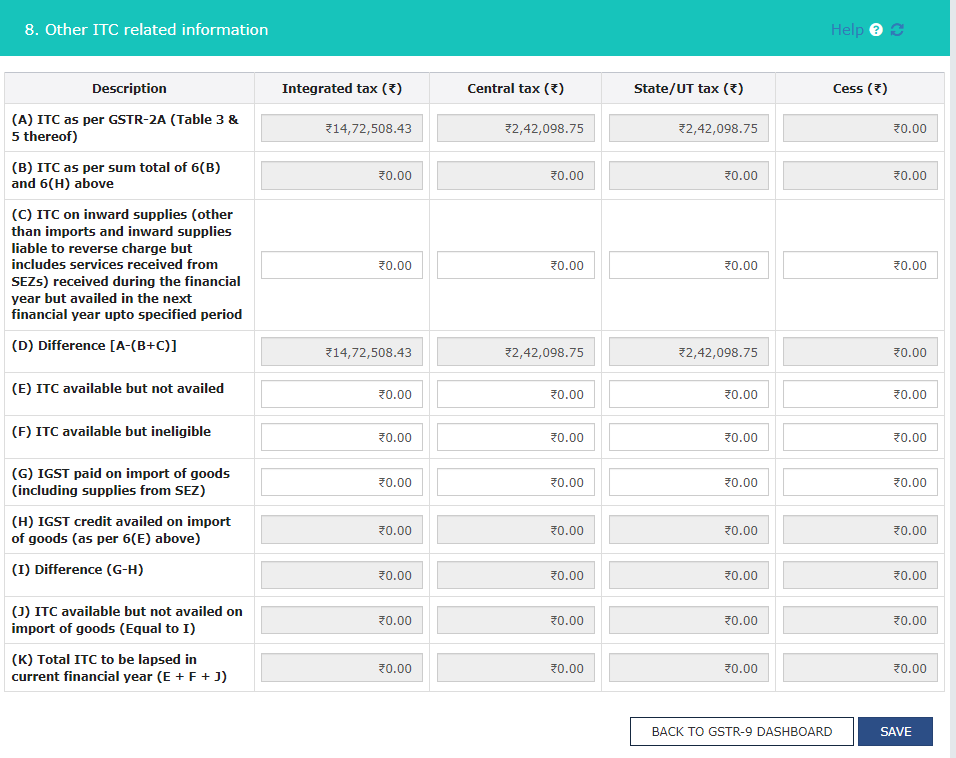

Table No. 8 - Other ITC Related Information

Point 8(A) ITC as per GSTR-2A (Table 3 & 5 thereof). - During the financial year 2022-23, inward supply has been received and the ITC available on it reflected in GSTR 2A is auto-populated and this cannot be edited.

Point 8(B) ITC as per sum total of 6(B) and 6(H) above- The sum-total from Table 6B and 6H of inputs, capital goods, and input services received as inward supply and ITC reclaimed as per the provisions of GST Act during the financial year is auto-populated.

Point 8(C) ITC on inward supplies (other than imports and inward supplies liable to reverse charge but includes services received from SEZs) received during the financial year but availed in the next financial year up to the specified period. - This involves ITC received during the financial year but availed in the next financial year in the specified time period.

For example – In F.Y.2022-23 ITC received. But was availed in the next financial year within the period specified under Section 16(4) of the CGST Act (i.e. April 2023 to September 2023 period ITC availed)

Point 8(D) Difference [A-(B+C)] – In Point 8(D), the difference [A - (B + C)] is auto calculated

A : ITC is auto-populated from GSTR 2A,

Less :

B : During the financial year we have received inputs, capital goods, and input services in the form of inward supply, and as per the provision of the GST Act, ITC has been reclaimed

C : ITC on inward supply received during the financial year but availed in the next financial year in the specified time period.

Point 8(E) ITC available but not availed- The credit which was available and not availed in FORM GSTR-3B shall be declared here.

Point 8(F) ITC available but ineligible- The credit which was available and the credit was not availed in FORM GSTR-3B as the same was ineligible shall be declared here.

Point 8(G) IGST paid on import of goods (including supplies from SEZ) - Aggregate value of IGST paid at the time of imports including imports from SEZs during the financial year shall be declared here.

Point 8(H) IGST credit availed on import of goods (as per 6(E) above) - ITC as declared in Table 6E will be auto-populated here.

Point 8(I) Difference (G-H) -

Point 8(J) ITC available but not availed on import of goods (Equal to I) - During the year we have import of goods and ITC is available on it but has not been availed. It is auto populate in Point J.

Point 8(K) Total ITC to be lapsed in the current financial year (E + F + J) - The total ITC which shall lapse for the current financial year shall be computed in this row.

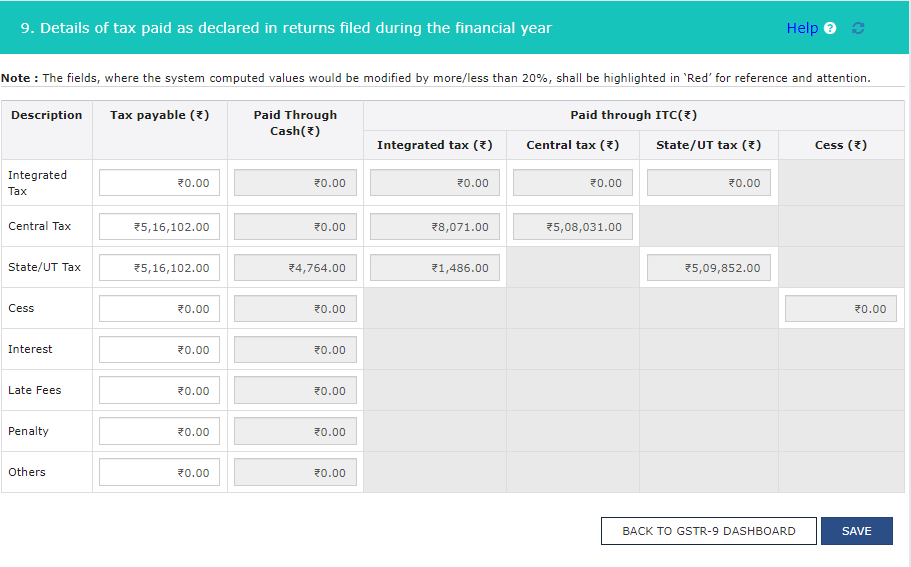

Part-IV Table No. 9 - Details of tax paid as declared in returns filed during the financial year.-

In Table No. 9 data is auto populated from GSTR 3B. This table is related to liability. This is a summarized form of tax-paid liability declared and payable and paid in cash or utilized through ITC during the year.

If we have a normal return then we do not have to make any changes here. But if differential tax is payable. Then, add the tax amount in the tax payable column.

If any differential tax is payable. Pay through Form DRC – 03 with interest. We can edit the tax payable column. But paid through cash and paid through ITC column cannot be edited.

Part-V. Particulars of the transactions for the financial year are declared in returns of the next financial year till the specified period.

In the current financial year, we declared details related to the previous year and the next financial year. Such details have to be submitted here.

For Example – In the current F.Y. 2022-23, we declared details related to the previous year 2021-2022 Or

Details of the current financial year 2022-23, declared in the period from April 2023 to September 2023 period. Such details have to be submitted here.

Table No. 10 - Supplies/tax declared through Amendments (+) (net of debit notes) -This table contains details of such supplies and taxes that have been declared through amendments. It is shown in the table only after the net of debit notes.

For Example - If you missed any sale and shown in the period from April 2023 to September 2023. Then details of such supply are to be furnished here.

Table No. 11- Supplies/tax reduced through Amendments (-) (net of credit notes) - This table contains details of supplies and taxes that have been reduced through amendments. It is shown in the table only after the net of credit notes.

Table No. 12- Reversal of ITC availed during the previous financial year- In this table, submit the details of ITC reversal which was availed in the previous financial year.

Table No. 13 -ITC availed for the previous financial year - In this table, Details of ITC availed in the previous financial year are required to be submitted.

Table No. 14 Differential tax paid on account of declaration in 10 & 11 above.

The details of the differential tax amount, which has come due to table numbers 10 & 11 have to be submitted here. Table 14 particularly related to, liability which was related to the financial year 2022-23. But declared and paid in the financial year 2023-24. In table 10- supplies tax declared through amendment, we increase the supplies and declare additional liability, and in table 11- supplies, tax reduced through amendment, we reduce the supplies and reduce additional liability.

If the net effect is an increase in liability and we have paid tax on it in the financial year 2023-24, then, it will be shown in table no. 14.

Similarly, if the interest amount is also paid, then, it will be shown in the interest column in table no.14.

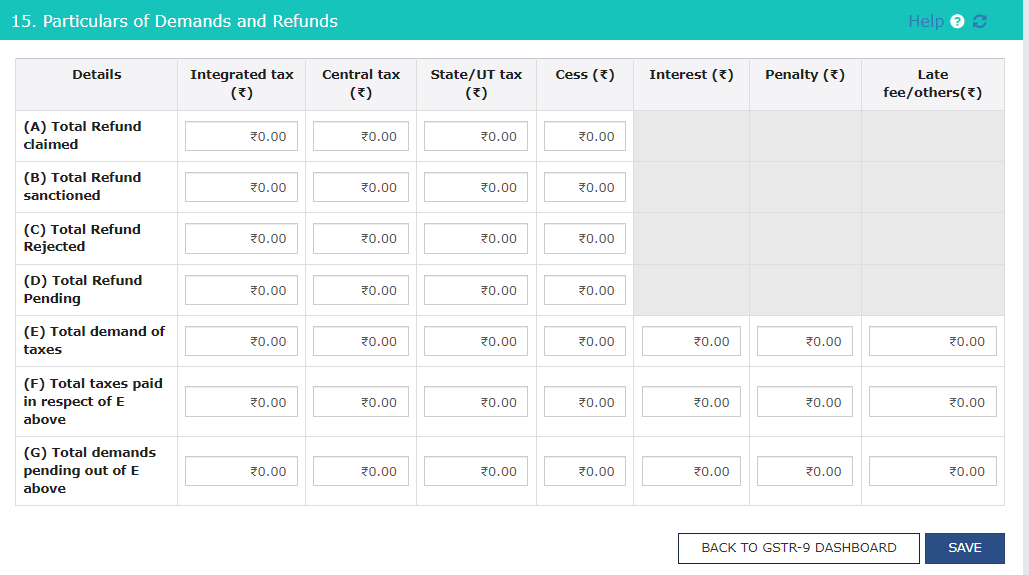

Part- VI - Other Information.

Point 15 (A) Total Refund claimed - In Point A, You have to declare the details related to the total refund claimed during the year.

Point-15(B) Total Refund sanctioned - In Point B, You have to declare the details related to the total refund sanctioned during the year.

Point-15(C) Total Refund Rejected - In Point C, You have to declare the details related to the total refund rejected during the year.

Point-15(D) Total Refund Pending - In Point D, You have to declare the details related to the total refund pending during the year.

Point-15(E) Total demand of taxes – In point E, you have to declare the details related to the Aggregate value of demands of taxes.

Point-15(F) Total taxes paid in respect of E above – In point F, you have to declare the details related to the Aggregate value of taxes paid out of the total demand of taxes.

Point-15(G) Total demands pending out of E above – In point G, you have to declare the details related to the Aggregate value of demands pending out of 15E above.

Table No. 16 Information on supplies received from composition taxpayers, deemed supply under section 143 and goods sent on an approval basis

Point 16(A) - Supplies received from Composition taxpayers - During the year Aggregate value of supplies received from composition taxpayers shall be declared here. Table 5 of FORM GSTR-3B may be used for filling up these details.

Point 16(B)-Deemed supply under Section 143- Aggregate value of all deemed supplies from the principal to the job-worker as per Section 143 of the CGST Act shall be declared here. We have to enter the amount in the taxable value. Also, the value of the respective integrated tax Central tax, and State tax has to be entered manually.

Point 16 (C) - Goods sent on an approval basis but not returned- Aggregate value of all deemed supplies for goods which were sent on an approval basis but were not returned to the principal supplier within 180 days of such supply shall be declared here. Also, the value of the respective integrated tax Central tax, and State tax has to be entered manually.

Table No. 17 - HSN Wise Summary of outward supplies.

If in the preceding financial year, turnover is more than Rs. 5 crores, then enter details of HSN-wise outward supply.

Table No. - 18 HSN Wise Summary of Inward Supplies.

Table No. 19- Late fee payable and paid.

Late fee will be applicable if an annual return is filed after the due date.

FAQs (Frequently Asked Questions)

Q : What is GSTR-9 Turnover limit?

A : GSTR-9 is an Annual return to be filled by every registered person whose aggregate turnover is more than Rs. 2 crore.

Q : What is GSTR-9 due date?

A : The due date to file GSTR-9 for a financial year is 31st of December of the following year

Q : What is GSTR-9 due date for FY 2022-23?

A : Due Date for filing of annual return for F.Y. 2022-23 is 31st December 2023.

Q : GSTR-9 late fees.

A : Late fee for not filing GSTR-9 within the due date is Rs. 200/- per day (CGST Rs.100/- and SGST Rs.100), subject to a maximum of 0.25 percent of the assessee’s Turnover in the State or Union Territory).

Disclaimer:-The information available on this website/ App is solely for informational purposes. We make no representation or warranties of any kind, express or implied about the accuracy, reliability, with respect to information and material or video available on website/APP, any reliance you place on such information is therefore strictly at your own risk. We are not liable for any consequence of any action taken by you relying on the material/information provided on this website/APP.

Checking Your Income Tax Refund Status [ ITR Refund Status ] : A Comprehensive Guide

If taxpayer income tax return is not received, In this guide, we'll walk you through the process of checking your income tax refund status for the fiscal year 2022-23 (Assessment Year 2023-24) after March 31, 2023. There are two convenient methods to track your refund:

1. Income tax Website

2. Through Customer Care

Process 1: Verify online via the Income Tax Department's website.

Option 1: Without Login

- Go to the Income Tax website.

- Under the "Quick link" tab, select the option "Know Your Refund Status."

- Enter your PAN and Assessment Year (2023-24), fill your Mobile Number for OTP verification, and click "Continue." to proceed further

- Then Enter the OTP received on your Mobile Number and click "Continue."& proceed further

- Your refund status will be displayed on the screen of your device.

Please Note: in case your refund due date is on or before March 31, 2023, check through the NSDL website for your ITR refund status.

Option 2: With Login on the e-Filing Portal

- Go to the e-Filing portal homepage.

- Enter your user ID and password.

- Direct to the e-File tab > Income Tax Returns > View Filed Returns.

- Check the refund status for the desired Assessment year. Click on "View Details" to track the life cycle of filed ITR.

Refund Status Codes:

- Status 1: Refund issued.

- Status 2: Refund partially adjusted.

- Status 3: Full refund adjusted.

- Status 4: Refund failed.

Note: For PAN-related issues, follow Aadhaar linkage instructions.

Process 2: Check via Customer Care

Call the Income Tax Department's customer care center at 1800-103-0025/ 1800 103 0025/1800 419 0025/ +91-80-46122000/+91-80-61464700 to inquire about your refund status.

Important Reminders:

- Refund processing may take up to 6 weeks. [ ITR Refund Time ]

- Validate your bank account, ensuring it matches PAN details.

- Verify the IFSC code and ensure your mentioned account is operational.

By following these steps, you can easily track your income tax refund status and stay informed about the processing stages.

ITR Refund Time

Income tax Refund processing by the tax department starts only after the return is e-verified by the taxpayer. Generally, it takes 4-5 weeks for the refund to be credited to the account of the taxpayer. However, if a refund is not received during this duration, the taxpayer must check for intimation regarding discrepancies in ITR; check email for any notification from the IT department regarding the refund. The taxpayer can also check refund status on the e-filing portal.

Disclaimer:-The information available on this website/Application is solely for informational purposes. We make no representation or warranties of any kind, express or implied about the accuracy, reliability, with respect to information and material or video available on website/Application, any reliance you place on such information is therefore strictly at your own risk. We are not liable for any consequence of any action taken by you relying on the material/information provided on this website/Application.

New Feature of “Discarded Return” introduce by Income Tax

Income tax Department has introduce the new function for Income Tax “Discarded Return” where a user Discarded a Return of income.

Key Condition for Discard Return

- Income tax should be filed u/s 139(1) /139(4) / 139(5).

- ITR status is “unverified” / “Pending for verification”

Option can be exercised for Income Tax returns that have been filed on or after April 1, 2023. This means it is applicable for the financial year 2022-23 (Assessment year 2023-24). you can only discard your IR return if it is not verified. In case you have sent your ITR verification to CPC and it has not reached it, the discard option can still not be exercised.

The benefit of such especially for those taxpayers who, after submitting the return, realized an error or omission in the tax return. Instead of first e-verifying the tax return and then revising it, they can now simply "discard" the unverified tax return and file a fresh return.”

How is Discard ITR different from Revised ITR?

Before introducing the Discard Income Tax Return option, a taxpayer realized that an error had been made. It is only after the verification of the ITR that one can go to the ITR portal to revise their tax return.

In case of discard ITR, not verified return, will be completely deleted from the Income Tax Portal. So, from a taxpayer’s perspective, it would entail filing a fresh return.

For example, you file your income tax return on July 27, but do not verify it. You discard the return on November 29 and then file a new income tax return. This new return would be treated as a belated return and would invite penal consequences since it would be filed after the original due date of July 31. However, if you have verified your ITR and then filed a revised return after July 31, then no penal consequences are applicable.

Income tax has issued FAQs for Discard Return

- Question 1: I filed my Original ITR u/s 139(1) on 30th July 2023 but not yet been verified. Can I Discard it?Response: Yes, user can avail the option of “Discard” for the ITRs being filed u/s 139(1) /139(4) / 139(5) if they do not want to verify it. The user is provided a facility to file an ITR afresh after discarding the previous unverified ITR. However, if the “ITR filed u/s 139(1)” is Discarded and the subsequent return is filed after the due date u/s 139(1), it would attract implications of belated return like 234F etc., Thus, it is advised to check whether the due date for filing the return u/s 139(1) is available or not before discarding any previously filed return.

- Question–2: I Discard my ITR by mistake. Is it possible to reverse it? Response:Response: No, if ITR is Discarded once, it can’t be reversed. Please be vigilant while availing Discarding option. If an ITR is Discarded, it means that such ITR is not filed at all.

- Question3: Where can I find the “Discard option”?Response: The user can find the Discard option in below path :

www.incometax.gov.in → Login → e-File → Income Tax Return → e-Verify ITR → “Discard” - Question 4: Is it mandatory to file subsequent ITR if I “Discarded” my previous unverified ITR?Response: A user, who has uploaded the return data earlier, but has made use of the facility to discard such unverified return is expected to file a subsequent ITR later on, as it is expected that he is liable to file the return of income by way of his earlier action.

- Question 5: I sent my ITR V to CPC and it is in transit and has not yet reached CPC. But I don’t want to verify the ITR as I get to know that details are not reported correctly. Can I still avail “Discard” option?Response: The user shall not discard such returns, where the ITR-V has already been sent to CPC. There is an undertaking to this effect before discarding the return.

- Question 6: When can I avail of this “Discard” option and can I avail of this “Discard” option multiple times or only once?Response: The user can avail of this option only if the ITR status is “unverified” / “Pending for verification”. There is no restriction on availing of this option multiple times. The precondition is “ITR status” is “Unverified” / “Pending for verification”.

- Question7: My ITR filed for AY 2022-23 is pending for verification. Can I avail of this “Discard” option?

Response: The user can avail this option only from AY 2023-24 onwards for the respective ITR. This option will be available only till the time limit specified for filing ITR u/s 139(1)/139(4) /139(5) (i.e., 31st December of respective AY as of now). - Question 8: I discarded my Original ITR 1 filed on 30th July 2023 on 21st August 2023 and I want to file subsequent ITR on 22nd August 2023. Which section should I select?Response: If the user discards the Original ITR filed u/s 139(1) for which the due date u/s 139(1) is over, they are required to select 139(4) while filing the subsequent returns. As there is no prior valid return exist, the date of the Original ITR / Acknowledgement number if Original ITR fields are not applicable. Further, if the user wants to file a revised return in the future, he needs to provide details of the “Original filing date” and “Acknowledgement number” of the valid ITR i.e., ITR filed on 22nd August 2023 for filing a revised ITR

Disclaimer:-The information available on this website/ App is solely for informational purposes. We make no representation or warranties of any kind, express or implied about the accuracy, reliability, with respect to information and material or video available on website/APP, any reliance you place on such information is therefore strictly at your own risk. We are not liable for any consequence of any action taken by you relying on the material/information provided on this website/APP.

What is casual income [Section 56(2)(ib)]

Casual income refers to earnings characterized by their spontaneous and unpredictable nature.

Characteristics of Casual Income

- Incidental

- Accidental

- Arises unexpectedly

- Not part of a planned or regular source

- Cannot rely on it’s consistency

Casual income means income in the nature of / Example of Casual Income

- Winning from lotteries,

- Crossword puzzles,

- Races including horse races,

- Card games and other games of any sort,

- Gambling/ betting, etc.

Casual income does not include :

- Capital gains, chargeable under the provisions of section 45; or

- Receipts arising from business or the exercise of a profession or occupation; or

- Receipts, by way of addition to remuneration of an employee, such as bonus, gratuity, perquisites, etc.

Casual and Non-recurring Income

Casual Income: These are the incomes about which the taxpayer remains uncertain before it is received such as example Income from a lottery, crossword competition, betting etc.

Non-recurring Income: These are the incomes that arise at an irregular interval. example gain on sale of assets, insurance claim.

Gift V/s Casual Income

Receipts which are of a casual and non-recurring nature will be liable to income-tax only if they can properly be characterised as "income" either in its general connotation or within the extended meaning given to the term by the Income-tax Act. Hence, gifts of a purely personal nature will not be chargeable to income-tax except when they can be regarded as an addition to the salary or when they arise from the exercise of a profession or vocation.

Circular : No. 158 [F. No. 173/2/73-IT(A-I)], dated 27-12-1974.

Tax Rate

Chargeable to tax at a flat rate of 30% under section 115BB

Other Point

- No expenditure is allowed as a deduction from casual income.

- The benefit of basic exemption limit is not available in respect of casual income.

- Deduction under Chapter VI-A is not allowable from such income.

Procedure of grossing up

In the case of resident individual or HUF, are as follows

- Lottery Income Received = Gross Lottery Income – TDS @ 30% on Gross Lottery Income.

- Lottery Income Received = 70% of Gross Lottery Income

- Gross Lottery Income = Lottery Income Received / 70%

- Note: Tax is not deducted in the following cases, hence, there is no need for grossing up.

- If the amount of winning from the lottery etc. or horse race is not more than Rs.10,000.

- In case of winning from racing other than horse race e.g. camel races, etc.

General

Winning from a motor car rally: Winning from a motor car rally is a return for skill and effort and cannot be treated as casual income but taxable as normal income

Lottery held as stock in trade: Winning from lottery to an agent or trader out of its unsold stock (tickets) shall be treated as incidental to the business and taxed under the head “Profits & gains of business or profession”

Disclaimer:-The information available on this website/Application is solely for informational purposes. We make no representation or warranties of any kind, express or implied about the accuracy, reliability, with respect to information and material or video available on website/Application, any reliance you place on such information is therefore strictly at your own risk. We are not liable for any consequence of any action taken by you relying on the material/information provided on this website/Application

What is GSTR-9C, its due dates and how to file GSTR-9C

What is GSTR-9C?

In GSTR-9C, reconciliation of the Annual Return (GSTR-9) and Audited Financial Statement is done and if all the details are reconciled then normally GSTR-9C has to be filed. But if there is any unreconciled amount, which creates a liability, it has to be paid and then the return has to be filed.

In which case GSTR-9C will be applicable, what is the turnover limit for GSTR-9C?

Registered persons, whose aggregate turnover exceeds Rs 5 crore are also required to file a Self-Certified Reconciliation Statement along with the Annual Return (GSTR-9). Before filing GSTR-9C, the taxpayer is required to file GSTR-9. i.e. GSTR-9C can only be filled when the taxpayer has filled GSTR–9.

Due date of GSTR-9C

The due date to file GSTR-9C for a financial year is 31st of December of the year following the relevant financial year.

Due date for the FY 2022-23 : The due date to file GSTR-9C for the Financial Year 2022-23 is 31st December 2023.

GSTR-9C has been divided into 4 parts :-

| Part –1 Basic details. |

| Part –2 Reconciliation of turnover declared in audited Annual Financial Statement with turnover declared in Annual Return (GSTR-9). |

| Part –3 Reconciliation of tax paid. |

| Part -4 Reconciliation of Input Tax Credit (ITC). |

In GSTR – 9C following items are reconciled:-

| Total Turnover |

| Taxable Turnover |

| Tax Paid |

| Input Tax Credit (ITC) |

Practical Guide to file GSTR-9C :-

GSTR–9C can be filed only through offline utility. To file GSTR-9C, the department provides an offline tool, through which taxpayers create JSON and then upload it on the GST portal. First of all, go to the GST website and download the offline GSTR-9C tool from offline tools in the download tab on the home page. To download, you have to click on the offline GSTR-9C tool and then click on download. If you proceed, the offline tool will be downloaded in a zip file. Now you have to extract that file and work in the Excel sheet of the offline tool. Before filing GSTR-9C, you have to file GSTR-9. Only after that, you can file the GSTR – 9C form.

Now let us understand how to file GSTR-9C with offline utility:

In PART-A, you have to submit basic details like GST No., Financial Year, Legal Name & Trade Name and also mention whether you are liable for audit under any other law (Companies Act, Income Tax etc.) If yes, then that applicable law will have to be mentioned.

Now, let us understand Part B:-

Pt. II. Reconciliation of turnover declared in audited Annual Financial Statement with turnover declared in Annual Return (GSTR9)

In this table, the turnover declared in the audited financial statement is compared with the turnover declared in the return (GSTR-9).

Point-A : Turnover (including exports) as per Audited Financial Statement for the State / UT (For multi-GSTIN units under the same PAN, the turnover shall be derived from the Audited Annual Financial Statements )*

In Point-A, turnover as per books of account is to be mentioned. But, if you are working in multiple states, then you will have to file separate GSTR-9C for each state and the turnover of books will also have to be calculated state-wise. This turnover is to be derived from the audited financial statement.

Example : Suppose, you have 2 branches, one is in MP and the other is in Gujarat.

Turnover Details of Branch :-

| MP Branch | Rs. 5.50 Cr |

| Gujarat Branch | Rs. 6.50 Cr |

| Total Turnover | Rs. 12.00 Cr |

If you are filing GSTR-9C of MP then only the turnover of MP i.e. Rs. 5.50 Cr will have to be mentioned in Point-A.

Point-B : Unbilled revenue at the beginning of the Financial Year

In Point-B, unbilled revenue has to be reported at the beginning of the financial year. This means that such bills are included in the turnover of last year's books as per the accounting standard. But, in GST, Tax payment is made according to the time of supply. Therefore, its GST is paid in the current year. By doing this, there will be a difference in the turnover of our books of account and annual return. In this case, Books of Account will show fewer sales this year and GST will show more sales. That difference has to be reported here.

Let us understand this point with an example –

In accounting, revenue recognition is done according to IND AS and in GST, Tax is paid according to the time of supply. Suppose, there was a bill that was recognized in the books of accounts in March 2022. But, if GST on it is payable in April 2022, then it will be shown in the return of April 22, due to which there will be a mismatch in the turnover of books and GST, then this difference has to be reported here in Point B.

Point-C : Unadjusted advances at the end of the Financial Year

In Point-C, the unadjusted advance has to be reported at the end of the year. If any advance is received then it is not recognized as revenue in the books as per accounting standards. But in the GST Act, if any advance is received above Rs 1000, then in such case, the applicability of GST arises. In this case, your current financial year turnover will show less in the books. But, there will be show sales shown in the annual return. That difference has to be reported here in Point-C.

Let us understand this point with an example –

Suppose, you received an advance related to service on 28th February 2022, which was billed in April 2022, on which GST was paid in March 2022, i.e. last year itself. So in this case, sales will show more in the books of account in the current FY 2022-23, but sales will show less in the annual return. That difference has to be reported here in Point-C.

Point-D : Deemed Supply under Schedule I

Transactions notified in Schedule I are reported in Point-D. Deemed supply is defined in this schedule. If more than one GST number is registered on the same PAN and any transaction is made between them, then it will be called deemed supply. This means that, even if it is your branch, but if you get a separate GST number on the same PAN, it is considered a distinct person and GST is charged even on transfer from one branch to another.

Let us understand this point with an example–

Suppose you have 2 branches, one is in MP and the other is in Gujarat. You sold goods worth Rs. 50 lakhs from the MP branch to the Gujarat branch. So in this case, you would have paid GST on Rs. 50 lakh. But, when you would have finalized the books of account, then this sale of Rs. 50 lakh would have been excluded from the total sales. By doing this there will be a difference in the turnover of our books of account and annual return. In this case, fewer sales will be shown in Books of Account and more sales will be shown in GST. That difference has to be reported here.

Point- E: Credit Notes issued after the end of the financial year but reflected in the annual return

Point-E is related to a Credit note which is issued after the end of the financial year but is included in the annual return. If we understand from the example, suppose you have made a sale on 30th March 2023, where the customer did not like the goods and the customer returned the goods. Whose credit note was issued by you on April-23. But, you have considered this credit note while filing your annual return. This means that your outward liability in your GSTR-9 has been reduced. But in books, a credit note will be shown only in April-23, due to which there will be more turnover in books in F.Y.2022–23, due to which there will be the difference in turnover of books and turnover of annual return which has to be reported in point-E.

Point-F: Trade Discounts accounted for in the audited Annual Financial Statement but are not permissible under GST

Point-F is related to trade discounts. Any trade discount given which is not allowed in GST. This means that, due to giving a trade discount, even if the sales in the books of account have reduced, but you will have to pay GST on the entire sales only. Because of this, the turnover in books of account reduces, but in GST this trade discount is not allowed due to which there is a difference between the turnover of GST and the turnover of books. That difference was reported here in point-F.

Point-G : Turnover from April 2017 to June 2017

Point-G Turnover from April-17 to June-2017, this point is applicable only for 9C of FY 2017-18. Because GST became applicable in July-2017. So in that case, more sales will be shown in the books of account for FY 17-18 and fewer sales will be shown in GST. That difference was reported here.

Point-H : Unbilled revenue as of the end of the Financial Year

In Point-B we understood about unbilled revenue at the beginning of the financial year, here in Point-H, the amount related to the end of the financial year has to be entered.

Meaning that such bills are included in the current year's turnover in the books of account. But, in GST, payment will be made according to the time of supply. Therefore, its GST payment is made in the next financial year. By doing this there will be a difference in the turnover of our books of account and annual return. In this case for the current year, there will be more sales in Books of Account and fewer sales will be shown in GST. That difference has to be reported here.

Let us understand this point with an example –

In accounting, revenue recognition is as per IND AS, and in GST, GST is paid as per the time of supply. So suppose there was a bill that was recognized in the books of accounts in March 2023. But, GST on it is payable in April-2023, due to which there will be a mismatch in the books and GST turnover of FY 2022-23, so this difference has to be reported here in Point-H.

Point-I : Unadjusted Advances as at the beginning of the Financial Year

In Point-I the unadjusted advance at the beginning of the year has to be reported. If any advance has been received in the last year, then as per the accounting standard it would not have been recognized in the books as revenue last year. But in the GST Act, if any advance of more than Rs.1000 is received then in such case, the applicability of GST comes only after the advance is received. In this case, your current financial year's turnover will show more in the books. But, the annual return will show less turnover. That difference has to be reported here in Point-I.

Let us understand this point with an example –

Suppose you have received an advance related to service on 28th February 2022, which was billed in April 2022, on which GST was paid in March 2022, i.e. last year itself. So in this case, sales will be shown more in the books of account in FY 2022-23, but the annual return will show less turnover. That difference has to be reported here in Point-I.

Point J : Credit notes accounted for in the audited Annual Financial Statement but are not permissible under GST

Point J is to report such credit notes that are related to the last financial year whose credit note has been issued and accounted for during the current financial year, but this credit note is not allowed or permissible in GST (For example, a credit note has not been issued before 30th November or return), then it will not be permissible in GST. Due to this your current year’s turnover will be reduced, but there will be no reduction in GST turnover, due to which a difference will be created and this difference will be reconciled by adding it to point J.

Point-K : Adjustments on account of supply of goods by SEZ units to DTA Units

Point K- is related to the adjustment of supply made from the SEZ unit to the DTA unit. Here it is important to understand that in reality it is a sale, but there is no need to report the sales made by SEZ in GST, due to which the turnover in books is higher and the GST turnover is lower. So to reconcile this difference, we reduce the supply of SEZ to DTA at point k, so that the turnover becomes equal to the annual return.

Point-L : Turnover for the period under the composition scheme

Point -L is related to the turnover of the composition scheme. For example, let us assume that in FY 2022-23, you were in the composition scheme from April-22 to June-22. After that you opted for the normal scheme. The turnover made in the composition scheme is not included in GSTR-9 (annual return). Due to this, in FY 2022-23, the turnover in the Book of Account will show more, but it will show less in the annual return, due to which a difference will be created and this difference will be reconciled by reporting it in point-L.

Point-M : Adjustments in turnover under section 15 and rules thereunder

In Point M, the adjustment of the difference in turnover of books and GST, due to section 15 of CGST (value of supply of goods & services) and its rules will have to be reported here.

In Books of Account, Transaction value (sales) is determined according to the Accounting Standard. However in GST, according to Section 15, transaction value is determined. Due to this, there may be differences in Books of Account and GST Turnover. This difference can be both positive/negative. You can add or reduce as per the situation.

If we understand from the example, for a certain transaction the transaction value in GST is Rs. 10,00,000/-, but according to the books of account the value is Rs. 12,00,000/-. So you have to mention 200000 in the negative at this point. Due to this GST and book of accounts turnover will be reconciled.

Point-N : Adjustments in Turnover due to foreign exchange fluctuation

The difference that has arisen due to foreign exchange fluctuations has to be reported in Point N. Due to foreign exchange fluctuations, there may be a difference in the Books of Account and GST Turnover. This difference can be both positive/negative. You can add or reduce as per the situation.

If you want to increase the turnover of books then you will have to enter the figure in positive and if you want to reduce the turnover then you will have to enter the figure in negative.

Point-O : Adjustment in Turnover due to reasons not listed above

In this point, apart from all the points discussed so far, if there is a difference between the annual return and the audited financial statement due to any other reason, then that difference has to be mentioned. This difference can be both positive/negative. You can add or reduce as per the situation.

Point P : Annual Turnover after adjustments as above(A+B+C+D-E+F-G-H-I+J-K-L+M+N+O)

According to the figure reported in points above, in point-P, the figure of automatically adjusted turnover will be shown.

Point-Q : Turnover as declared in Annual Return (GSTR9)

In Point Q, the turnover declared in the Annual Return (GSTR – 9) has to be mentioned.

Point-R : Un-Reconciled turnover (Q- P)

After making all the adjustments, your audited annual turnover should match with the turnover mentioned in GSTR – 9 (annual return). If there is any difference, it will be shown here.

Reasons for Un - Reconciled difference in Annual Gross Turnover :-

After making all the adjustments, if there is a difference between the audited annual turnover and the turnover mentioned in GSTR – 9 (annual return), then you have to mention the reason here why your turnover is mis-match.

In this table, reconciliation is done between the taxable turnover of the books of account and the annual return.

Point-A : Annual Turnover after adjustments [from 5(P) above]

This figure is auto-populated from the work done in the previous tables.

The adjusted turnover that has come after making various adjustments in the previous table is shown here.

Point-B : Value of Exempted, Nil Rated, Non-GST Turnover, No supply turnover

In this point Exempted, Nil Rated, Non-GST Turnover, and No Supply Turnover have to be mentioned.

Point-C : Zero-rated supplies without payment of tax

In this Point-C, zero-rated supply without payment of tax has to be mentioned.

Point-D : Supplies on which tax is to be paid by the recipient on a reverse charge basis

In this Point-D, the amount of supplies on which the recipient has paid tax in the reverse charge mechanism has to be mentioned.

Point-E : Taxable turnover as per adjustments above (A-B-C-D)

After entering the amount in the above points, the taxable turnover is auto-calculated and shown in this table. Points B, C & D are deducted from Point A.

Point-F : Taxable turnover as per liability declared in Annual Return (GSTR-9)

Here the taxable turnover declared in the annual return has to be mentioned in this point.

Point-G: Unreconciled Taxable Turnover (F-E)*

If there is a difference in turnover, it will be auto-calculated and shown here and the reason will have to be mentioned in the next Excel sheet.

This table is of unreconciled taxable turnover. If your taxable turnover is not reconciled, then you will have to mention the reason here.

This table is of reconciliation of tax paid, in this reconciliation of rate rate-wise liability has to be done. All the rates are given in this table in which you have to enter the taxable value and taxes as per the books and do reconciliation with the tax amount paid as declared in GSTR-9 and if there is any difference, then its reason has to be mentioned in the next Excel sheet.

In this sheet, if there is any difference between the taxes paid as per the books and the tax amount paid as declared in GSTR-9, the reason for the same has to be mentioned.

In this table, additional liability has to be shown which has arisen due to a difference in turnover, or difference in taxable turnover, or difference in tax paid. This means you have paid less to the Government and this amount will have to be paid in cash.

This table is of reconciliation of input tax credit.

In Point-A, you have to mention the ITC of the state for which you are filing GSTR-9C from the audited financial statement.

In Point-B, such ITC has to be mentioned which has been booked in the previous financial year but claimed in this financial year.

In Point-C, ITC has to be mentioned which has been booked in the current financial year but will be claimed in the subsequent financial year.

In Point-D, the ITC availed in the audited financial statements or books of account will be auto-populated here.

In Point-E, you have to mention the ITC claimed in GSTR-9 (annual return).

Point-F : If there is a difference between the ITC claimed in the annual return and the ITC as per books of account, it will be shown here. If there is any difference, then its reason has to be mentioned in the next sheet and if you have claimed excess ITC, then you have to pay it.

If ITC cannot be reconciled, then its reason will have to be mentioned in this sheet.

This table is optional, here you have to give bifurcation of expense-wise ITC as declared in books and mention the declared ITC in the annual return. If there is any difference between the two, the reason for the difference has to be mentioned in the next table.

If ITC cannot be reconciled, then its reason will have to be mentioned in this sheet.

In this sheet, any additional liability that is payable due to a difference in ITC has to be mentioned along with interest and penalty.

This is the last table of GSTR-9C. The additional liability arises due to a lack of reconciliation in the books of account and the annual return has to be mentioned in this sheet and in this sheet, the rate-wise value and GST amount have to be mentioned. Along with that, interest and penalty also have to be mentioned.

Whatever liability has arisen, will have to be paid through DRC-03.

After this, you have to click on the Home sheet. From here, you can generate the PDF, take a preview, and re-check it from your records. After verifying all the details, you will have to create JSON by clicking on the option to create a JSON file.

After creating the JSON file, you will have to login in the GST portal.

After login, in the service menu, click on annual return in user services.

After that, the financial year for which you want to file an annual return will have to be selected from the drop down menu

After that, the financial year for which you want to file an annual return will have to be selected from the drop down menu

After that, in the tab of GSTR-9C, this JSON file will have to be uploaded, and then it will have to be verified with DSC and submitted. In this way, GSTR-9C will be filed.

Disclaimer:-The information available on this website/ App is solely for informational purposes. We make no representation or warranties of any kind, express or implied about the accuracy, reliability, with respect to information and material or video available on website/APP, any reliance you place on such information is therefore strictly at your own risk. We are not liable for any consequence of any action taken by you relying on the material/information provided on this website/APP.

Introduction:

Dividend is a share of a company's profits & retained earnings distributed to shareholders. When a company earns profit, it can choose either to reinvest earnings for future growth or pay dividends to shareholders. Generally, the decision is proposed by the board of directors and approved by Shareholders considering financial performance, cash flow, and future plan.

Dividends are not Expenses

It's a distribution of profits it's not classified as an expense and no deduction from income allowed.

Dividends & Income Tax

Dividend, commonly associated with the distribution of profits by a company to its shareholders, takes on a broader definition under Section 2(22) of the Income-tax Act in India.

I. Definition of Dividend [U/s 2(22)]:

The Income-tax Act expands the scope of dividend to include the following situations:

(a) Distribution of Accumulated Profits:

- Any distribution of accumulated profits by a company to its shareholders, whether in cash or in kind, is deemed as dividend. In the case of in-kind distribution, the market value of the assets released is considered as dividend.

(b) Distribution of Debentures, Deposit Certificates, and Bonus Shares:

- Distribution of debentures, deposit certificates, or bonus shares by a company to its shareholders is treated as dividend to the extent of the company's accumulated profits. The market value of bonus shares is deemed as dividend in the hands of preference shareholders.

(c) Distribution on Liquidation:

- Any distribution to shareholders during a company's liquidation/ closing, attributable to accumulated profits before liquidation, is deemed as dividend.

(d) Distribution on Reduction of Capital:

- Distribution to shareholders by a company on the diminution /reduction of its capital, to the extent of accumulated profits, is treated as dividend.

(e) Loan or Advance by a Closely Held Company:

- Any loan or advance by a closely held company to a shareholder, beneficially owning 10% or more of the voting power, is deemed as dividend to the extent of accumulated profits. The same applies to loans or advances to specified concerns in which a qualifying shareholder has a substantial interest.

Loans granted in the ordinary course of business, forming a substantial part of the company's business, are not deemed as dividend. - Repayment of a loan or charge of interest at market rate does not alter the applicability of Section 2(22)(e).

Other Exceptions: - Distribution in respect of non-participating shares issued for full cash consideration. - Payment on buyback of shares in accordance with Section 77A of the Companies Act, 1956. - Distribution of shares on demerger by the resulting company.

II. Basis of Charge of Dividend [Section 8]:

- Dividend declared at the annual general meeting is considered the income of the shareholder in the year of declaration.

- Deemed dividends under Section 2(22)(a) to (d) are treated as income in the year of distribution.

- Advance or loan deemed as dividend under Section 2(22)(e) is considered income in the year of payment.

III. Head of Dividend Income [Section 56(2)(i)]:

- Dividend income is taxable under the head "Income from other sources." However, shares held for trading purposes may be taxed under the head "Profits and gains of business or profession."

IV. Tax on Dividend Income:

- Dividend income received by a resident from a company, whether domestic or foreign, is taxable at normal rates of tax.

- The tax rates on dividend income for various categories of assesses, including non-resident persons, foreign portfolio investors (FPIs), non-resident Indian citizens (NRIs), and investment divisions of offshore banking units, are outlined under different sections of the Income-tax Act. Here's a summary of the relevant sections and tax rates:

| Section | Assessee | Particulars | Tax Rate |

| 115AC | Non-resident | Dividend on GDRs of an Indian Company or PSU purchased in foreign currency | 10% |